Most people think about the interest rate and the EMI amount of the loan or credit card before borrowing. But one important factor that often gets ignored is the hard inquiry credit score impact. Many people are unaware of the fact that making multiple inquiries for a loan can actually lower their credit score by a little bit.

It is always a good idea to know about the hard inquiry credit score so that you can make the best out of your borrowing options. In the following sections, we will be discussing the impact of hard inquiries, the difference between hard and soft inquiries, and the way you can make the most out of them.

What Is a Hard Inquiry Credit Score?

Let’s first answer the common question

Hard inquiry occurs when a lender performs a credit check after a borrower applies for a loan, credit card, or any other credit product.

The term hard inquiry credit score refers to the impact this credit check has on your overall score.

Whenever you apply for:

- Personal loan

- Home loan

- Car loan

- Credit card

- Business loan

The lender conducts a hard inquiry to assess your creditworthiness.

It is different from checking your own credit score, which does not affect your score.

Why Do Lenders Conduct Hard Inquiries?

A lender has to assess:

- Your repayment history

- Outstanding loans

- Credit utilization

- Previous defaults

- Total number of recent applications

A hard inquiry will enable them to assess the risks involved in lending you money.

You can be considered a high-risk borrower if you have many loan applications.

Hard Inquiry vs Soft Inquiry

Some borrowers are not aware of the difference between a hard and soft inquiry. Here is a simple comparison:

| Feature | Hard Inquiry | Soft Inquiry |

| Triggered By | Loan/credit application | Checking your own score |

| Permission Required | Yes | No |

| Impact on Score | Yes (temporary drop) | No impact |

| Visible to Lenders | Yes | No |

| Duration on Report | Up to 2 years | May not be visible |

Soft inquiries happen when:

- You check your own credit score

- A lender pre-approves you

- Background checks occur

Soft checks are safe and do not affect your score.

How Hard Inquiries Affect Credit Score

Now let’s understand how hard inquiries affect credit score over time.

A single hard inquiry usually reduces your credit score by:

- 3 to 5 points (on average)

If your credit score is 750, it can fall to 745 or 747.

However, if you make many loan applications in a short period, your score can fall significantly.

For example:

| Number of Hard Inquiries (in 6 months) | Possible Score Impact |

| 1 inquiry | -3 to -5 points |

| 2–3 inquiries | -5 to -10 points |

| 4–6 inquiries | -10 to -20 points |

| 7+ inquiries | Significant risk signal |

While the drop may seem small, lenders look at patterns. Frequent applications may indicate that you’re financially stressed or that you’re a “credit-hungry” individual.

How Long Does a Hard Inquiry Stay on Your Report?

The hard inquiry may remain on your credit report for 2 years or less. However:

- Its impact reduces after 6–12 months

- After one year, the effect becomes minimal

The most important period is the first 6 months.

That is why spacing out loan applications is important.

Does Every Hard Inquiry Reduce Score?

Not always significantly.

If:

- You have a strong credit history

- Low outstanding debt

- No recent defaults

Then one hard inquiry will have very minimal impact.

However, if your score is already low, multiple hard inquiries can worsen your situation.

Multiple Loan Applications: Why It’s Risky

Suppose you apply to five different lenders within one week.

Each lender performs a hard inquiry.

This may signal that:

- You are urgently seeking funds

- You were rejected elsewhere

- You may be over-leveraged

Even if you get approved, your credit score may temporarily decline.

This is why understanding the hard inquiry credit score concept is crucial before applying everywhere at once.

Special Case: Rate Shopping

There is one exception.

If you apply for the same type of loan (like a home loan) within a short time frame (usually 14–45 days depending on the bureau), credit bureaus may treat multiple inquiries as a single inquiry.

This allows borrowers to compare interest rates without heavy penalties.

However, this grouping rule may vary, so apply cautiously.

Real-Life Example

Let’s say:

Credit Score: 760

You apply for:

- 1 credit card

- 2 personal loans

- 1 consumer durable loan

Within 30 days, you may see a drop of 10–15 points.

If you continue paying EMIs on time, your score may recover within a few months.

How to Minimize Hard Inquiry Impact

Here are simple steps to protect your credit score:

1. Check Eligibility First

Use eligibility calculators before formally applying.

2. Avoid Multiple Applications

Do not apply to many lenders at once.

3. Maintain Good Credit History

Strong payment history reduces inquiry impact.

4. Space Out Applications

Keep at least 3–6 months gap between major loan applications.

5. Improve Your Credit Score Before Applying

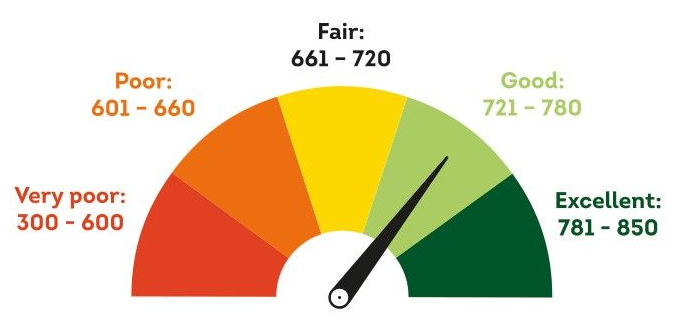

If your credit score is less than 700, it is better to improve your score before applying for a loan.

How Digital Platforms Handle Credit Checks

Currently, there are digital platforms that allow borrowers to have their credits evaluated immediately. Some platforms, such as Olyv and other fintech platforms, may allow borrowers to know if they’re eligible before the final approval.

Even if the process is now digital and convenient for borrowers to have their credits evaluated, it is still important to remember that making a loan application may mean that a hard inquiry will be made on your credit report.

Convenience should not replace careful planning.

Common Myths About Hard Inquiry Credit Score

Myth 1: Checking My Own Score Reduces It

False. Self-check is a soft inquiry.

Myth 2: One Hard Inquiry Destroys Your Credit Score

False. One inquiry has minimal impact.

Myth 3: Hard Inquiries Remain on File Forever

False. They remain for 2 years, but the effect occurs earlier.

Myth 4: Rejection of a Loan Affects the Credit Score

It is not the loan rejection that affects the score, but the inquiry.

When to Worry?

You should worry when:

- You have more than 4–5 inquiries in 6 months

- Your score is below 650

- You plan to apply for a large loan (like home loan) soon

Too many recent inquiries can reduce approval chances.

Why Credit Discipline Matters

Your credit score shows:

- Financial stability

- Repayment behavior

- Risk level

Proper management of hard inquiry credit scores helps to secure better interest rates and approval of loans.

Even small variations in hard inquiry credit scores can affect eligibility for loans.

Final Thoughts

Understanding what is a hard inquiry credit score helps you borrow smartly. A hard inquiry is a credit check carried out by a lender after a loan or credit card application is made. Though a single hard inquiry does not affect a credit score significantly, applying for several credit products in a short span of time can lower a credit score and raise red flags for lenders.

Knowing how hard inquiries affect credit score allows you to:

- Plan loan applications carefully

- Avoid unnecessary rejections

- Maintain a healthy credit profile

Before applying for credit, check your eligibility, compare options wisely, and space out applications.

A good credit score opens doors to better financial opportunities. Managing hard inquiries responsibly ensures those doors remain open.