Many people check their credit score but do not understand what it actually means. You might see a number like 682 or 755, but what does it mean in terms of your financial status? More importantly, how does it impact your loan approval, EMI, and credit limit?

Understanding the meaning of the credit score categories can help you make better financial choices. In this blog, we will discuss the official credit score rating scale in India, how the various levels of credit score classification work, and how each credit score category can impact your financial choices.

What is a Credit Score?

A credit score is a three-digit number that indicates your creditworthiness. It indicates to lenders how well you have managed borrowed funds in the past.

In India, credit scores typically range between 300 and 900. The higher the credit score, the less risky you are to lenders.

However, rather than simply looking at the number, lenders might be interested in knowing what credit score category you belong to.

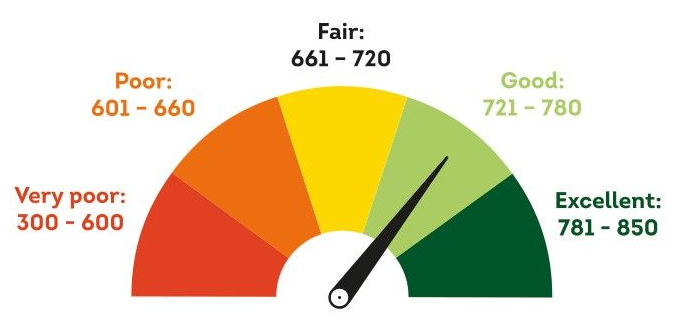

Understanding Credit Score Categories in India

Let’s break down the standard credit score rating scale used by most financial institutions in India.

| Credit Score Range | Credit Score Classification | Category Meaning | Loan Approval Chances |

| 750 – 900 | Excellent | Very low risk borrower | Very High |

| 700 – 749 | Good | Low risk borrower | High |

| 650 – 699 | Fair | Moderate risk | Possible but stricter terms |

| 550 – 649 | Poor | High risk | Difficult |

| 300 – 549 | Very Poor | Very high risk | Rare approval |

This table shows how lenders interpret different credit score categories. Your score determines how easily you can borrow and at what cost.

What Each Credit Score Category Means for You

Let’s understand these classifications in simple words.

1. Excellent (750 – 900)

This is the strongest credit score category.

If your score falls here, you may enjoy:

- Quick loan approvals

- Lower interest rates

- Higher loan amounts

- Minimal documentation

- Better negotiation power

- Higher credit card limits

Borrowers in this credit score classification are considered financially disciplined. Banks compete to offer them better deals.

2. Good (700 – 749)

This is still a strong category.

You can expect:

- High approval chances

- Competitive interest rates

- Standard documentation

- Decent loan eligibility

While not perfect, this level on the credit score rating scale still puts you in a comfortable position.

3. Fair (650 – 699)

This is a moderate category.

Here’s what it usually means:

- Loan approval is possible

- Interest rates may be slightly higher

- Stricter verification process

- Lower credit limits

- Possible need for additional income proof

You may still qualify for loans, but lenders will evaluate your profile more carefully.

4. Poor (550 – 649)

This credit score category signals risk.

You might face:

- Higher interest rates

- Lower loan amounts

- Frequent rejections

- Need for a guarantor

- Secured loan preference

Improving your score becomes very important at this stage.

5. Very Poor (300 – 549)

This is the weakest category in the credit score classification system.

At this level:

- Loan approvals are rare

- High rejection rates

- Only secured loans may be possible

- Very high interest costs if approved

Immediate credit improvement steps are necessary.

How Credit Score Categories Affect Your EMI

Your category directly impacts how much EMI you pay.

Let’s take an example:

Loan Amount: ₹5,00,000

Tenure: 3 Years

| Credit Score Category | Interest Rate (Approx.) | EMI | Total Interest Paid |

| Excellent (780) | 10% | ₹16,134 | ₹80,824 |

| Good (720) | 12% | ₹16,607 | ₹97,852 |

| Fair (670) | 15% | ₹17,347 | ₹1,24,492 |

| Poor (600) | 20% | ₹18,579 | ₹1,68,844 |

The difference between excellent and poor categories can be nearly ₹88,000 extra interest.

This shows clearly how important understanding credit score categories is.

Why Lenders Use Credit Score Classification

Lenders use the credit score rating scale to:

- Assess repayment risk – Credit score helps them understand the borrowers repayment capacity and provide a suitable loan based on the profile.

- Decide loan amount eligibility – Different lenders have different eligibility criteria for loan approval. However, credit score is considered as one of the important factors to decide how much loan amount can be approved for the borrower. Borrowers with high scores are eligible for faster loan approval.

- Set interest rates – Lenders consider higher credit score and provide lower interest rates, whereas borrowers with low credit score are provided loans with higher interest rates.

- Approve or reject applications – Considering the above factors, it is important to maintain a high credit score to avail various offers and easy loan approval. Lower credit score always indicates risk in loan approval

- Determine credit card limits – Credit score number also indicates your credit utilization behaviour. It helps the lender to decide whether you are capable of providing higher credit card limit or not.

It helps them make quick and consistent decisions.

For borrowers, knowing your credit score classification helps you prepare before applying for credit.

Factors That Decide Your Credit Score Category

Your score is calculated based on:

- Payment history (on-time payments matter most)

- Credit utilization ratio

- Length of credit history

- Type of credit (secured vs unsecured)

- Number of recent loan applications

Small financial habits make a big difference in which category you fall into.

How to Move to a Better Credit Score Category

If you are in the fair or poor category, don’t worry. Improvement is possible.

Here are simple steps:

- Pay EMIs and credit card bills on time

- Keep credit usage below 30%

- Avoid applying for multiple loans together

- Do not delay minimum due payments

- Check your credit report for errors

- Maintain old credit accounts responsibly

With consistent discipline, you can gradually move up the credit score rating scale.

How Digital Platforms Help Track Categories

Today, many financial platforms allow users to check and monitor their credit score regularly. Some platforms like Olyv provide credit tracking features that help borrowers understand where they stand and what steps they can take to improve.

Monitoring your score regularly helps you:

- Know your current category

- Avoid surprises during loan application

- Plan borrowing better

- Improve financial awareness

It is not about just checking the number, rather it’s about understanding your credit score categories and acting accordingly.

Why Understanding Credit Score Categories Is Important

Here’s why this knowledge matters:

- It helps you apply at the right time.

- It reduces loan rejection chances.

- It improves negotiation power.

- It lowers borrowing costs.

- It helps you plan large purchases wisely.

- It strengthens long-term financial stability.

Instead of randomly applying for loans, you make informed decisions based on your credit score classification.

Final Thoughts

Many borrowers see their score but don’t understand what the categories truly mean. The credit score rating scale is not just a number system, it is a financial grading structure that influences your approval chances, EMI burden, and overall borrowing power.

Understanding credit score categories helps you take control of your financial journey. Whether you are planning a personal loan, home loan, or credit card, knowing your category ensures you are better prepared.

Your credit score is like a financial report card. The higher your position on the credit score classification scale, the easier and cheaper borrowing becomes.

Keep monitoring it, improve it step by step, and let it work in your favor whenever you need financial support.